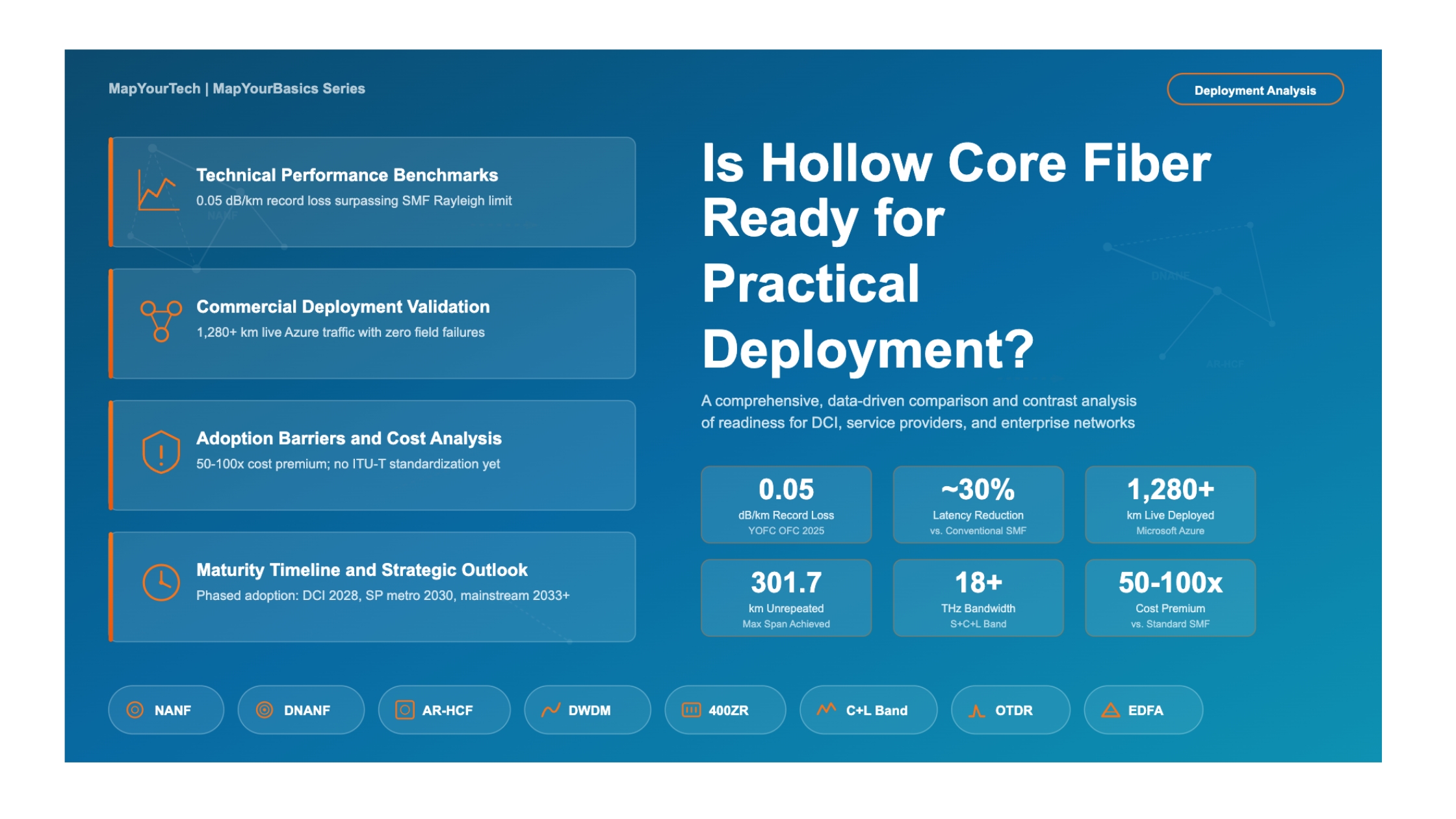

Is Hollow Core Fiber Ready for Practical Deployment?

A comprehensive, data-driven analysis of HCF's technical maturity, commercial readiness, adoption barriers, and the projected timeline for operational maturity across DCI, service provider, and enterprise networks.

1. Introduction

Hollow Core Fiber (HCF) represents one of the most significant innovations in optical transmission media since the development of low-loss single-mode fiber in the 1970s. By guiding light through an air-filled core rather than solid glass, HCF offers a fundamentally different approach to optical signal propagation, one that promises near-vacuum-speed transmission, near-zero nonlinear effects, and the potential to surpass the Rayleigh scattering limit that has bounded conventional fiber attenuation for decades.

As of early 2026, HCF has crossed several technical milestones that would have seemed impossible just five years ago. The record attenuation has fallen to 0.05 dB/km, surpassing the best conventional SMF. Microsoft has deployed over 1,280 km carrying live Azure customer traffic with zero field failures. AWS has begun production deployments connecting approximately 10 data centers, marking the entrance of a second hyperscaler into the HCF arena. Financial trading networks have operated HCF production routes for more than four years. Manufacturing partnerships between Microsoft-Corning-Heraeus and Relativity Networks-Prysmian are rapidly scaling production capacity. VIAVI has launched the industry's first all-in-one HCF testing and certification solution. Yet the technology still serves under 0.1% of global fiber installations, and costs remain 50-100x higher than standard single-mode fiber.

This analysis examines the full picture: the technical readiness, the commercial realities, the deployment challenges, and the timeline for HCF to achieve operational maturity for data center interconnect (DCI), service provider networks, and broader enterprise deployment.

2. The Verdict: Conditionally Ready

Summary Verdict

HCF is technically proven and commercially deployed for specific, high-value applications (high-frequency trading, hyperscale DCI, AI acceleration). It has achieved Technical Readiness Level 9 (TRL 9) for these niche use cases. However, it is not yet ready for general-purpose service provider or enterprise deployment due to cost barriers (50-100x premium), lack of ITU-T standardization, limited supply chain, and specialized operational requirements. The technology will likely remain confined to premium applications through 2028-2030, with broader DCI adoption in the late 2020s and service provider use in the early 2030s.

3. Technical Performance: HCF vs. SMF

The performance advantages of HCF over conventional single-mode fiber are not incremental improvements but fundamental physical differences arising from guiding light in air rather than glass. The table below provides a direct, quantitative comparison of the two technologies across every critical performance parameter.

| Parameter | Conventional SMF (G.652) | Hollow Core Fiber (AR-HCF) | HCF Advantage |

|---|---|---|---|

| Attenuation (C-Band) | 0.14 - 0.20 dB/km | 0.05 - 0.11 dB/km (record/lab) 0.085 - 0.28 dB/km (deployed) |

Surpasses Rayleigh limit of glass |

| Latency | ~4.9 µs/km | ~3.35 µs/km | 1.54 µs/km saving (~31% reduction) |

| Group Refractive Index | ~1.468 | ~1.003 | Light travels at 99.7% of vacuum speed |

| Chromatic Dispersion | ~17 ps/nm·km | ~2-4 ps/nm·km | 4-8x lower; reduces DSP complexity |

| Nonlinear Coefficient | ~1.3 W-1km-1 | ~0.001 W-1km-1 | ~1000x lower; enables higher launch power |

| Splice Loss | <0.05 dB (routine) | 0.04-0.16 dB (HCF-HCF) 0.15-0.3 dB (HCF-SMF) |

SMF still superior; HCF rapidly improving |

| Bandwidth | C+L band (~10 THz) | 18+ THz (S+C+L or broader) | 1.8x wider usable spectrum |

| Damage Threshold | ~1-2 W continuous | >3 W demonstrated (34.8 dBm) | Enables ultra-high-power transmission |

| Temperature Sensitivity | ~7.5 ppm/°C (Shupe constant) | ~0.52 ppm/°C | 14x better thermal stability |

| Cost per Meter | $0.10 (volume) | $5-10 (current commercial) | SMF vastly cheaper (50-100x) |

Table 1: Comprehensive performance comparison of Hollow Core Fiber vs. standard Single-Mode Fiber

4. Attenuation Evolution: The Record-Breaking Journey

The attenuation trajectory of HCF tells the story of a technology that has undergone one of the most dramatic performance improvements in optical fiber history. From losses exceeding 1,000 dB/km in early tubular anti-resonant fibers to the recent 0.05 dB/km achieved by YOFC at OFC 2025, the improvement spans more than four orders of magnitude within roughly two decades.

The critical inflection point came with the development of Nested Anti-Resonant Nodeless Fiber (NANF) structures, first proposed in 2014 and rapidly refined thereafter. The Double-Nested NANF (DNANF) architecture, adding a second layer of anti-resonant elements, provided the final breakthrough needed to push attenuation below the Rayleigh scattering limit of silica (~0.14 dB/km). This is not merely an engineering achievement; it represents a fundamental shift in which fiber type sets the benchmark for optical transparency.

| Wavelength / Band | Record Attenuation (dB/km) | Fiber Type | Institution |

|---|---|---|---|

| 1550 nm (C-Band) | 0.05 | AR-HCF | YOFC |

| 1560 nm (C-Band) | 0.174 | DNANF | Univ. of Southampton |

| 1550 nm (C-Band) | 0.11 | DNANF | Univ. of Southampton |

| 1625 nm (L-Band) | 0.22 | NANF | Univ. of Southampton |

| 1300 nm | 0.22 | DNANF | Univ. of Southampton |

| 850 nm | 0.33 | DNANF | Univ. of Southampton |

| 660 nm (Visible) | 2.85 | NANF | Research (Surface Scattering Reduction) |

Table 2: Record-low attenuation achievements in Hollow Core Fiber across key wavelengths

5. Deployment Readiness Scorecard

To provide a clear assessment of where HCF stands across every dimension required for practical deployment, the following scorecard rates each factor on a 1-10 scale based on the evidence gathered from commercial deployments, research publications, and industry reports.

6. Challenges Blocking Mainstream Adoption

6.1 Manufacturing Complexity and Cost

The fabrication of HCF requires an intricate arrangement of tiny glass capillaries or membranes around a hollow center, with wall thicknesses of approximately 500 nm maintained with micron-scale precision over tens of kilometers. This stack-and-draw process is far more sensitive to defects than conventional fiber drawing, resulting in lower yields and higher costs. Current commercial pricing of $5-10 per meter versus $0.10 per meter for high-volume SMF creates a 50-100x cost differential that cannot be justified outside of premium applications.

Microsoft has invested in expanding manufacturing capacity at the 40,000 sq ft Romsey facility, with partnerships announced with Corning (US production) and Heraeus Covantics (European production). Chinese manufacturer YOFC has also demonstrated production-grade capability. However, achieving the economies of scale needed to close the cost gap will require massive capital investment and sustained demand growth over the next 5-10 years.

6.2 Splicing and Connectorization

This remains perhaps the most critical practical barrier. The large hollow core (17-24 µm mode field diameter vs. 10.4 µm for SMF-28) creates significant mode field mismatch at connection points. Standard fusion splicing can cause collapse of the delicate microstructure at high temperatures, leading to catastrophic signal loss. While specialized splicers like Furukawa's FITEL S185PMROF with Ring-of-Fire technology have achieved median splice losses of 0.05 dB, these are specialized tools not yet widely available. Mode field adapters using GRIN lens designs have reduced HCF-to-SMF interface loss from 1.0-2.0 dB down to 0.15-0.21 dB in the lab, but field performance remains higher.

6.3 Standardization Gaps

No ITU-T recommendations exist equivalent to the mature G.652/G.654/G.655/G.657 series for conventional fiber. This leaves each manufacturer with proprietary, incompatible designs. Test equipment, installation procedures, certification programs, and warranty frameworks remain undeveloped. The technology cannot scale without industry standards enabling multi-vendor networks.

6.4 Operational Ecosystem Gaps

Beyond the fiber itself, several ecosystem elements are still maturing: field personnel training barely exists outside specialist contractors working for Microsoft and euNetworks; the hollow channels are vulnerable to contamination from dust and moisture requiring cleanroom-like handling of fiber ends; and bend sensitivity requires larger bend radii compared to SMF, impacting deployment in space-constrained environments.

Strengths Supporting Deployment

- 30%+ latency reduction proven in production over 3+ years

- Attenuation now surpasses SMF's fundamental limit

- Compatible with existing DWDM/400ZR transceivers

- Virtually zero nonlinear effects enable higher launch power

- 18 THz+ bandwidth vs. ~10 THz for SMF

- Enhanced intrusion detection for security-sensitive networks

- Demonstrated unrepeated transmission over 301.7 km

Barriers to Mainstream Deployment

- 50-100x cost premium over conventional fiber

- No ITU-T standards for specifications or testing

- Limited manufacturing supply chain (expanding: 5-6 facilities globally by mid-2026)

- Specialized splicing equipment and expertise required

- Larger bend radius than SMF (space constraints)

- Dust/moisture contamination risk at fiber ends

- No standardized training or certification programs

- Serves <0.1% of global fiber installations

- Demand exceeds supply (confirmed by AWS, February 2026)

7. Who Is Adopting HCF Today?

HCF adoption follows a clear tiered pattern, starting with sectors where the value of microsecond-level latency improvement vastly exceeds the cost premium.

| Adopter Category | Key Players | Primary Use Case | Deployment Stage | Justification |

|---|---|---|---|---|

| High-Frequency Trading | euNetworks, Jump Trading, Anova, McKay Brothers, BSO, DRW | Ultra-low latency exchange connectivity | Full Production (3+ years) | Microsecond advantages generate millions in revenue |

| Hyperscale Cloud | Microsoft Azure, AWS; Google and Meta evaluating | DCI for AI/ML workloads; AZ interconnect | Production (two hyperscalers live) | Competitive advantage + geographic flexibility + AI workload acceleration |

| Telecom Operators | China Mobile, China Telecom, BT, Comcast | Metro/DCI, 5G fronthaul | Trial / Early Production | Future-proofing; evaluating technical feasibility |

| Data Center Operators | Digital Realty/Interxion, lyntia, Equinix (evaluating) | Low-latency interconnects | Trial / Limited Deployment | Premium latency services for HFT/cloud clients |

| Defense / Government | DARPA (COUGAR program), Honeywell | Fiber optic gyroscopes, secure comms | R&D / Advanced Prototyping | 20x Faraday effect reduction; intrusion detection |

| Enterprise / General SP | Not yet adopted | N/A | Not started | Cost prohibitive; awaiting standardization |

Table 3: HCF adoption landscape by sector

8. Commercial Deployment Case Studies

8.1 Microsoft Azure (Dominant Global Deployment)

Microsoft's acquisition of Lumenisity in December 2022 transformed HCF from a niche supplier product to a core component of hyperscale cloud infrastructure. The flagship deployment connects two Azure data centers in a major European city via diverse metro routes exceeding 20 km each. Hybrid cable design incorporates 32 hollow core strands plus 48 single-mode fiber strands per cable, supporting multi-Tb/s DWDM capacity. By early 2026, Microsoft has deployed over 1,280 km of live Azure HCF with zero field failures, and the Azure team has measured 0.091 dB/km transmission loss across 1,200 km of production fiber — the lowest operational loss ever recorded.

In September 2025, Microsoft announced a major manufacturing scale-up through strategic partnerships with Corning and Heraeus Covantics. Corning will produce Microsoft's DNANF design at its North Carolina facilities, while Heraeus will manufacture at sites in both Europe and the US. This creates a multinational production supply chain essential for scaling HCF globally. Microsoft's stated goal is to deploy 15,000 km by late 2026, which would represent over 75% of global HCF installations. Azure engineers are working alongside both partners to transfer manufacturing IP, deliver training programs, and drive yield improvements required for industrial-scale production.

8.2 euNetworks (Financial Trading Pioneer)

euNetworks operates approximately 87+ km across multiple routes exclusively serving financial trading customers through the euTrade platform. Their deployment timeline demonstrates progressive confidence in the technology: starting with the world's first commercial deployment connecting Interxion LON1 to the London Stock Exchange in April 2021, expanding to 7 km to LSE's Docklands facility in March 2022, then 14 km connecting ICE's Basildon data center in September 2022, and reaching 40 km end-to-end in January 2023. The January 2025 deployment in Bergamo, Italy connecting Euronext represents their longest-ever deployment. All installations carry live production traffic delivering 1G to 10G services with 30%+ latency reduction.

8.3 China Mobile (First Telco Commercial Line)

China Mobile launched China's first commercial HCF line in July 2025, connecting Shenzhen and Hong Kong for cross-border financial transactions. The 20 km deployment achieved 0.085 dB/km average loss, 0.05 dB self-splicing, under 0.3 dB HCF-to-SMF connections, and single-wavelength throughput of 114.9 Tbit/s with over 30% latency optimization. Deployment during Typhoon Mawar validated robustness under extreme environmental conditions including severe flooding and outdoor splicing in high humidity.

8.4 AWS (Second Hyperscaler Enters Production)

AWS publicly confirmed its production deployment of hollow core fiber in late 2025, making it the second hyperscaler after Microsoft to move HCF into live infrastructure. According to AWS VP for Core Networks Matt Rehder, the company is deploying HCF to connect approximately 10 data centers, with plans for significantly expanded deployment as manufacturing capacity scales. AWS showcased its proprietary HCF cross-section at re:Invent 2024, revealing a design with loss characteristics similar to standard single-mode fiber — enabling selective insertion of HCF into existing fiber routes without requiring wholesale equipment changes.

The primary use case for AWS is long-distance availability zone (AZ) interconnect. AWS AZs are composed of multiple data centers that customers treat as one logical facility, requiring latency under roughly 0.5 milliseconds. This constraint limits how far apart facilities can be, and HCF's 30% latency reduction directly expands the viable search area for land and power. AWS confirmed that its HCF is compatible with existing optical equipment, though routes require approximately 10-20% more amplifiers than standard fiber — a gap expected to narrow as manufacturing quality improves. Rehder stated plainly that AWS wants more HCF than it can currently get, with demand significantly exceeding available supply. As part of a $200 billion capital expenditure plan for 2026, AWS is channeling significant investment into networking infrastructure including HCF.

8.5 Other Notable Deployments

Comcast conducted the first US ISP deployment in April 2022 with 40 km of hybrid HCF in Philadelphia, demonstrating 10-400 Gbps bidirectional transmission. China Telecom demonstrated 1.2 Tbit/s single-wavelength transmission over 20 km in July 2024 at 3W launch power. The Madrid trial by lyntia, Nokia, OFS, and Digital Realty in February 2024 achieved 600 Gbps capacity with 30% latency improvement over 1.386 km. Researchers at the University of Southampton demonstrated unrepeated transmission over 301.7 km with a total system data rate of 25.6 Tb/s.

8.6 Deployment Timeline

9. Vendor and Ecosystem Landscape

| Company | Type | HCF Technology | Strategy | Status |

|---|---|---|---|---|

| Microsoft / Lumenisity | Vertically Integrated User | DNANF (Double-Nested ARF) | Internal Azure deployment; vertical supply chain with Corning & Heraeus manufacturing | Production (1,280+ km deployed; 15,000 km target by late 2026) |

| AWS (Amazon) | Hyperscaler User | Proprietary HCF design | Long-distance AZ interconnect; working with multiple fiber vendors; $200B CapEx plan for 2026 | Production (~10 DCs connected; scaling aggressively) |

| Lightera (formerly OFS) | Furukawa | Merchant Supplier | Photonic Bandgap (AccuCore HCF) | Turn-key solution with factory termination and installation support | Commercial product; multiple deployments |

| Relativity Networks | Startup / Merchant Supplier | Anti-Resonant HCF (UCF CREOL) | DCI market; co-manufacturing with Prysmian at Eindhoven; ~$11M total funding with Prysmian investment | Production (deployed with US hyperscalers) |

| Prysmian Group | Cable Manufacturer + Investor | AR-HCF (via Relativity partnership) | Mass production at dedicated Eindhoven facility; equity investor in Relativity Networks | Manufacturing partnership active; production ramping |

| YOFC | Fiber Manufacturer | AR-HCF (Proprietary design) | Record performance (0.05 dB/km); domestic Chinese market + exports | Production-grade capability |

| Corning | Incumbent Fiber Giant | DNANF (manufacturing for Microsoft) | HCF production at North Carolina facilities under Microsoft IP; leveraging existing fiber infrastructure | Manufacturing (production for Microsoft) |

| Heraeus Covantics | Quartz & Silica Specialist | DNANF (manufacturing for Microsoft) | HCF production at US and European sites; preform and tube fabrication expertise | Manufacturing (production for Microsoft) |

| Linfiber Technology | Chinese Manufacturer | AR-HCF | Pluggable connectors; China Mobile deployment partner | Production-grade (deployed in Shenzhen) |

| Hengtong Optic-Electric | Chinese Fiber Manufacturer | AR-HCF | Expanding into HCF production for Chinese and international markets | R&D / Early production |

| VIAVI Solutions | Test & Measurement | N/A (Testing equipment) | Industry-first HCF testing solution: bidirectional OTDR, PMD, CD, AP on OneAdvisor 800 platform | Commercial product (Jan 2026); validated with 3 hyperscalers |

| Furukawa Electric | Equipment Manufacturer | N/A (Splicer manufacturer) | Specialized HCF splicers (S185PMROF, S185EVROF) with Ring-of-Fire technology | Commercial equipment available |

Table 4: Key players in the HCF ecosystem

10. Market Projections and Cost Trajectory

Market forecasts for HCF vary widely depending on assumptions about manufacturing scale-up and adoption pace, but all agree on strong growth from a small base. The most optimistic projections suggest the global HCF market could expand from approximately USD 420 million in 2024 to USD 3.17 billion by 2033 (CAGR of 27.4%). More conservative estimates project growth from around USD 132 million in 2023 to USD 916 million by 2032 (CAGR ~24%). At the most conservative end, some analysts project only 6.6% CAGR reaching ~$20 million by 2033.

The cost trajectory is the single most important factor determining adoption speed. Current pricing of $5-10 per meter must decline by at least an order of magnitude before HCF can compete outside of premium applications. However, the pace of cost reduction is accelerating beyond earlier projections. Key cost reduction drivers now include: Microsoft's 15,000 km deployment commitment and Corning/Heraeus manufacturing partnerships providing industrial-scale production; AWS entering as a second major buyer with demand exceeding available supply; Prysmian's dedicated HCF manufacturing facility at Eindhoven and equity investment in Relativity Networks; Chinese manufacturing competition from YOFC, Hengtong, and Linfiber; and the emergence of standardized test equipment (VIAVI) that reduces deployment costs. AWS VP Matt Rehder confirmed that HCF achieving general cost parity with conventional fiber is, in his view, "an inevitability" — though timing depends on manufacturing scale-up.

Cost Parity Estimate: Industry analysts project that HCF will reach cost parity with premium conventional fiber (G.654.E) for targeted DCI applications by approximately 2032-2035, assuming manufacturing volumes increase 10-20x from current levels. General cost parity with standard G.652 fiber is not expected before 2035-2040 at the earliest.

11. Maturity Timeline: When Will HCF Be Operationally Ready?

The path to full operational maturity for HCF can be broken into distinct phases based on application domain, each with different readiness requirements and timelines.

| Timeframe | Milestone | Target Application | Key Enablers |

|---|---|---|---|

| 2024-2026 | Multi-hyperscaler production maturity | HFT, Hyperscale DCI (Microsoft, AWS) | Microsoft 15,000 km target; AWS ~10 DC production deployment; Corning/Heraeus manufacturing; VIAVI test platform; Prysmian/Relativity scaling |

| 2026-2028 | Multi-vendor DCI evaluation + expansion | Premium DCI for cloud/AI operators (Google, Meta expected to evaluate) | Multiple production supply chains; first ITU-T study groups; standardized testing tools; Eindhoven production ramping |

| 2028-2030 | Standardized DCI deployment | Broader DCI; tier-1 service provider trials | ITU-T recommendations; cost reduction to $1-2/m; standardized splicing; third-party test ecosystem mature |

| 2030-2033 | Service provider metro adoption | Metro/regional latency-sensitive routes | Multi-vendor interoperability; trained workforce; cost approaching $0.50/m |

| 2033+ | Mainstream deployment | Long-haul, submarine (potential); general metro | Full cost parity; mature supply chain; complete standardization |

Table 5: HCF operational maturity timeline

12. HCF for Data Center Interconnect (DCI)

Data center interconnect represents the highest-probability near-term growth market for HCF outside of financial trading. The business case for HCF in DCI is driven by three converging factors.

First, geographic flexibility: HCF enables data centers to be separated by up to 90 km while maintaining latency equivalent to 60 km of conventional fiber. This 2.25x increase in viable geographic area is critical for hyperscalers seeking to locate facilities near available power sources rather than being constrained to dense urban areas where power is increasingly scarce.

Second, AI workload acceleration: Neural network training and inference require rapid, reliable transport of massive datasets. HCF's lower latency and elimination of fiber nonlinearities enable faster GPU-to-GPU communication across distributed clusters, directly reducing training time and improving real-time inference performance.

Third, capacity headroom: HCF's virtually zero nonlinear effects allow significantly higher launch power (demonstrated at 3W/34.8 dBm) without stimulated Brillouin scattering or four-wave mixing. Combined with 18+ THz of usable bandwidth, this provides substantial capacity headroom for future traffic growth.

DCI Readiness Assessment

For premium DCI applications where latency value exceeds cost premium, HCF is operationally ready today with support from specialized vendors. Both Microsoft (1,280+ km with zero failures) and AWS (~10 data centers) are running HCF in production, providing strong evidence of reliability and compatibility with existing DWDM infrastructure. For cost-sensitive DCI where HCF must compete with conventional fiber on economics, operational readiness is expected by 2028-2030, contingent on cost reduction to $1-2 per meter and the availability of standardized tools and training. The emergence of VIAVI's certified HCF testing platform in early 2026 addresses a critical gap in the deployment toolchain.

13. HCF for Service Providers

Service provider adoption of HCF faces a steeper path to maturity than DCI, primarily because service providers operate under stricter cost constraints, require multi-vendor interoperability, and depend on standardized operations at scale. The current absence of ITU-T recommendations, certified installation procedures, and broadly available field personnel training means that service providers cannot yet deploy HCF under their normal operational models.

However, several developments signal growing service provider interest. China Mobile's commercial 20 km Shenzhen-Hong Kong deployment in July 2025 marks the first true telco commercial application. AWS's confirmation that Google and Meta are also evaluating HCF suggests that demand from hyperscalers will drive manufacturing scale that eventually benefits service providers. The January 2026 launch of VIAVI's standardized HCF test and certification platform — the first all-in-one solution covering bidirectional OTDR, PMD, CD, and attenuation profiling — addresses a critical gap in the operational toolchain. Analysys Mason predicts that larger-scale deployment within core networks will occur in the late 2020s/early 2030s. For 5G/6G fronthaul and backhaul, HCF's negligible chromatic dispersion (~2-4 ps/nm·km vs. 17 ps/nm·km for SMF) and 20-30x better phase stability make it attractive for beamforming and phased-array applications.

Service Provider Readiness Assessment

Service providers should begin lab evaluation and limited field trials in 2026-2028 to build institutional knowledge and operational confidence. Targeted deployment on latency-critical metro routes could begin by 2029-2031, starting with routes where specific business services (financial connectivity, AI interconnect) justify the premium. General metro and regional deployment is unlikely before 2032-2035, when cost, standardization, and supply chain maturity are expected to reach acceptable thresholds.

14. Strategic Recommendations

For Hyperscale Cloud Operators

HCF is ready for strategic deployment today, validated by two major hyperscalers in production. Microsoft's 1,280+ km zero-failure track record and AWS's active deployment across ~10 data centers provide conclusive evidence of production reliability. Operators should evaluate HCF for new DCI routes where latency-sensitive AI/ML workloads or geographic flexibility for power access justify the premium. Multiple supply chain options now exist: Lumenisity/Microsoft, Lightera (formerly OFS), Relativity Networks/Prysmian, and Chinese manufacturers YOFC and Hengtong. VIAVI's January 2026 launch of the first all-in-one HCF testing platform — validated with three hyperscalers — addresses a key operational gap. Note that demand currently exceeds supply; early engagement with manufacturers is recommended to secure allocation.

For Financial Trading Firms

HCF is a proven, production-grade solution for exchange connectivity. Firms not yet using HCF on latency-critical routes are at a measurable competitive disadvantage. The 3 µs/km round-trip savings translates directly to trading performance. Contact euNetworks (Europe) or evaluate direct procurement from Lightera (formerly OFS) or Relativity Networks/Prysmian for North American routes.

For Tier-1 Service Providers

Begin lab evaluation now. Establish internal HCF competency by partnering with vendors for controlled trials on non-production routes. Participate in ITU-T standardization efforts to influence specifications. Plan for targeted deployment on premium latency-sensitive services by 2028-2030, but do not commit to large-scale infrastructure replacement before standardization and cost reduction milestones are met.

For Enterprise Network Operators

HCF is not yet ready for general enterprise deployment. Monitor cost trajectory and standardization progress. Plan evaluation cycles for 2030+ when multi-vendor availability and standardized operations are expected to mature. In the meantime, evaluate whether specific latency-sensitive applications (real-time analytics, algorithmic trading, remote surgery) could justify early premium deployment.

15. Conclusion

Hollow Core Fiber has crossed the most fundamental technical thresholds: it now surpasses conventional fiber's attenuation limit, it has been validated in multi-year production deployments carrying live traffic, and it has demonstrated compatibility with the existing coherent DWDM ecosystem. The question is no longer whether HCF works; it is whether the surrounding ecosystem of manufacturing, standardization, training, and supply chain can mature fast enough to enable deployment beyond a few well-funded early adopters.

As of early 2026, the answer has shifted decisively. Two hyperscalers — Microsoft and AWS — are now running HCF in production. Industrial manufacturing partnerships between Microsoft-Corning-Heraeus and Relativity Networks-Prysmian are actively scaling production capacity. VIAVI has delivered standardized testing tools validated by three hyperscalers. Google and Meta are reported to be evaluating the technology. AWS has stated publicly that demand for HCF exceeds current supply, and that general cost parity is "an inevitability." The pace of ecosystem development has accelerated well beyond what was projected even 12 months ago.

For premium DCI and financial trading, HCF is operationally ready today. For broader DCI serving cloud and AI workloads, readiness will arrive in the 2028-2030 timeframe as costs decline and multi-vendor options mature. For general service provider and enterprise deployment, the 2032-2035 horizon remains realistic, contingent on ITU-T standardization, workforce development, and at least a 10x cost reduction from current levels.

The strategic implications are clear: organizations that begin building HCF competency now will hold a significant advantage when the technology reaches mainstream readiness. The question for decision-makers is not whether HCF will transform optical networking, but whether their organization will be ready when it does.

References

- ITU-T Recommendation G.652 - Characteristics of a single-mode optical fibre and cable.

- euNetworks, "euNetworks deploys Lumenisity Limited CoreSmart hollowcore fibre cable in London."

- Microsoft Azure Blog, "How hollow core fiber is accelerating AI."

- Y. Chen et al., "Hollow Core DNANF Optical Fiber with <0.11 dB/km Loss," Proc. OFC'24, Th4A.

- YOFC, "Supporting-tube hollow core fiber achieves 0.05 dB/km loss over 21.7 km," OFC 2025.

- Analysys Mason, "Hollow-core fibre for low latency and increased bandwidth: the next game-changer in optical cables."

- Charlotte Forster et al., "The Deployment of Hollow Core Fiber," Microsoft TechCommunity.

- OFS Furukawa, "AccuCore HCF Fiber Optic Cable Assembly."

- Prysmian Group / Relativity Networks Partnership Announcement, March 2025.

- Unrepeated HCF Transmission over spans up to 301.7 km, ECOC 2024.

- Microsoft Azure, "Microsoft Azure scales Hollow Core Fiber (HCF) production through outsourced manufacturing," September 2025.

- Fierce Network, "AWS wants more hollow core fiber than it can get," January 2026.

- AWS Blog, "Building resilience: Inside AWS's nine million kilometers of fiber-optic cabling," November 2025.

- VIAVI Solutions, "VIAVI Announces Industry's First Long-Range Hollow Core Fiber Bidirectional Testing and Certification Solution," January 2026.

- Prysmian Group, "Prysmian Invests in Relativity Networks to Establish a Long-Term Partnership," July 2025.

- Data Center Knowledge, "AWS Networking Boss Talks Roadmap, Hollow Core Fiber," February 2026.

- Sanjay Yadav, "Optical Network Communications: An Engineer's Perspective" - Bridge the Gap Between Theory and Practice in Optical Networking.

Developed by MapYourTech Team

For educational purposes in Optical Networking Communications Technologies

Note: This guide is based on industry standards, best practices, and real-world implementation experiences. Specific implementations may vary based on equipment vendors, network topology, and regulatory requirements. Always consult with qualified network engineers and follow vendor documentation for actual deployments.

Feedback Welcome: If you have any suggestions, corrections, or improvements to propose, please feel free to write to us at [email protected]

Related Articles on MapYourTech